How Mariah Carey Turned $9 Million into $35 Million

By Lantern Finance

Hey Lantern Community!

You're probably hearing "All I Want for Christmas Is You" on repeat everywhere you go. But here's what most people don't know about her:

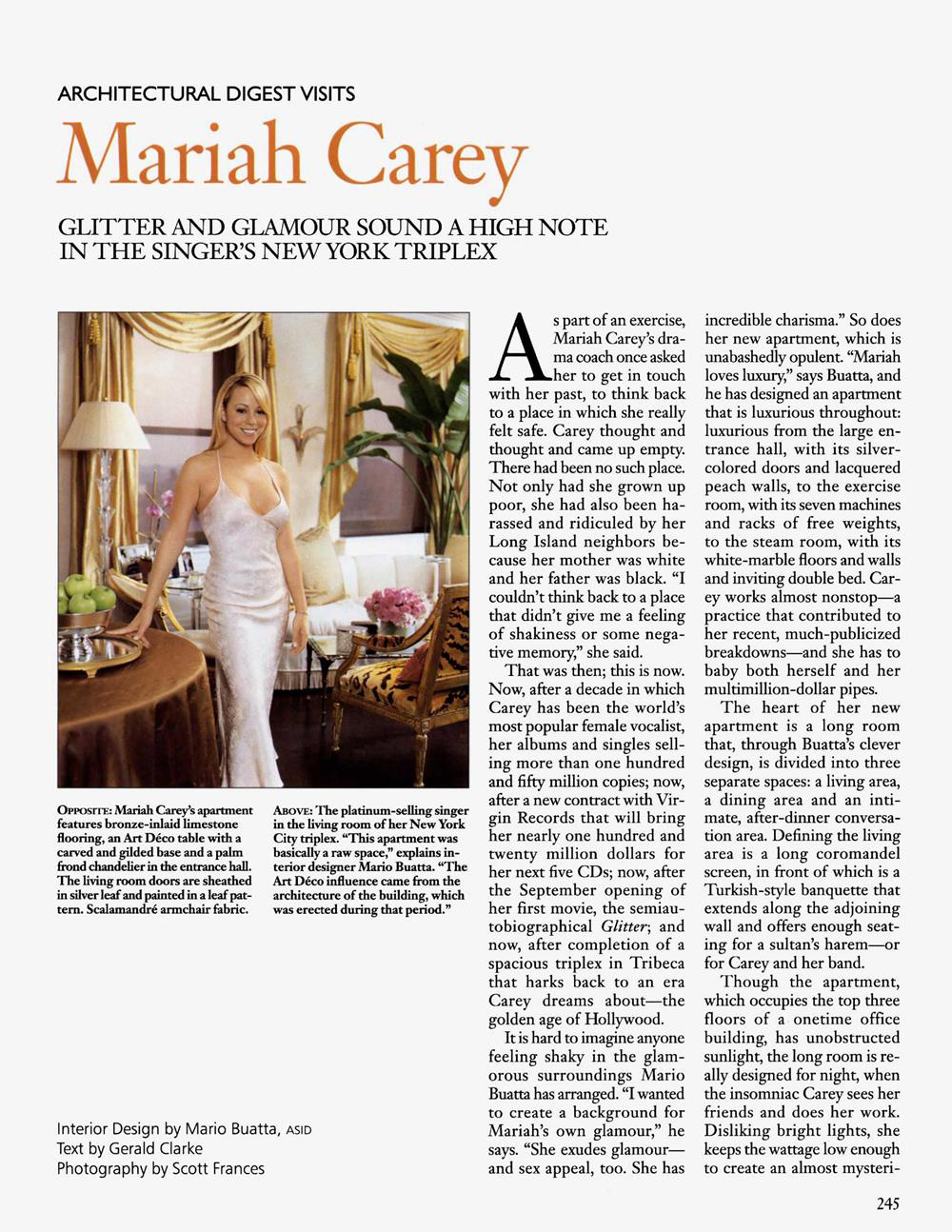

Mariah Carey bought a NYC penthouse for $9 million in cash back in 1999.

Architectural Digest, 2001

Today it's worth $30-35 million.

But here's the thing. She didn't just let it sit there appreciating. She borrowed against it. Repeatedly.

Today, we’ll take a closer look at how the Queen of Christmas pulled this off.

But first, market update!

She used her penthouse like a personal ATM

While "All I Want for Christmas" generates billions of listens and $2.5+ million every holiday season, Mariah was playing an even smarter game with her real estate.

Mariah's moves:

Bought the penthouse outright for $9 million in 1999

Combined it with the unit below to create a trophy triplex

Watched it appreciate to $30-35 million over 25 years

Borrowed over $18 million against it through strategic refinancing

Never sold her asset

The result? She pulled out $18+ million in liquidity while still owning a property worth double that amount.

The refinancing timeline (aka "How to pull out $18M from one property")

1999: Bought for $9M cash

2009: First major loan - $8M from JPMorgan Chase

Real estate values recovered from the 2008 crash. Time to access some equity.

2015: Second loan - $2.6M from City National Bank

Borrowed another $2.6M (paid off in 2016). Asset kept appreciating.

2016: Big refinance - Upsized to $17.6M

Refinanced the original JPMorgan loan and pulled out roughly $9.6 million in cash.

2018: Another upsize - Increased to $18.6M

Borrowed an additional $1 million more.

Net result: Pulled out roughly $18.6 million from a property she still owns that's now worth $30-35 million.

Why tabloids say she's "in debt" (and why they might be wrong)

Yes, Mariah has $18.6 million in mortgage debt.

But she also has an asset worth $30-35 million.

Her equity position: $11-16 million (and growing as Tribeca real estate continues to appreciate)

The headlines screaming about her "massive debt" miss the entire point. This could be strategic leverage.

Here's what financial advisors actually say:

Mortgage rates during her refinancing period: 3-5% (historically cheap debt)

Mortgage interest is tax-deductible for those who itemize

If she can earn higher returns elsewhere (music catalog, business ventures, investments) than her after-tax mortgage rate, this is a positive carry (aka borrow cheap debt, and invest into higher yielding investments to make the difference)

This means she's likely making money by maintaining the mortgage, provided she makes wise investment choices.

The Mariah playbook for regular people:

Never sell appreciating assets

Borrow against them instead

Use cheap debt strategically

Let your assets keep working for you

Maintain liquidity for opportunities

You don't need a $35 million penthouse or a Christmas anthem that generates millions.

You just need appreciating assets (like crypto) and a platform that lets you borrow against them smartly.

At Lantern, we make it simple:

No credit checks

Same-day funding

Interest-only payments

No liquidation fees

Your crypto stays safe with BitGo while you access liquidity

Want to see what this looks like for you?

Text us: (415) 365-0100 or check our calculator: https://lantern.finance/borrow

Keep your assets. Borrow smart. And maybe put on some holiday music while you're at it.

The Lantern Team

This newsletter is for educational purposes only and does not constitute financial advice. Always consult with your financial advisor before making lending decisions.